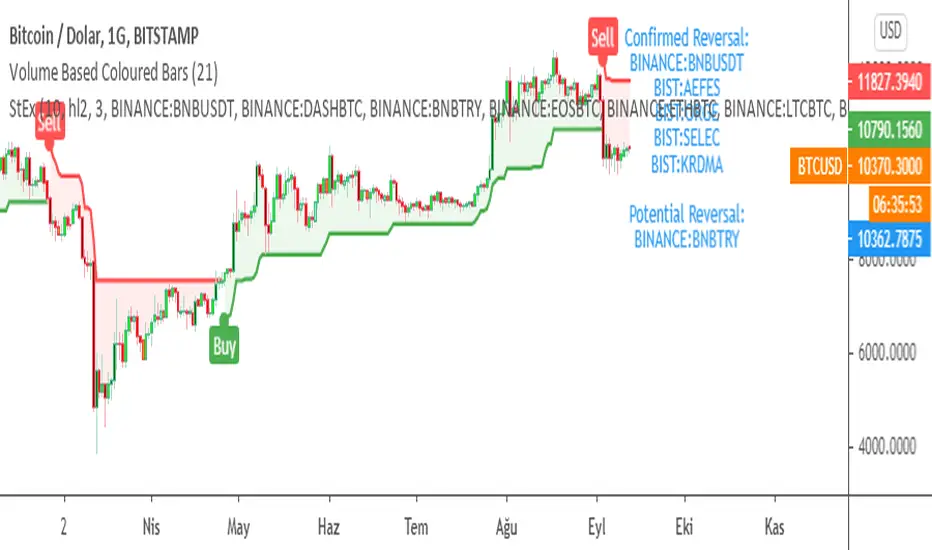

SuperTrend EXPLORER / SCREENERSUPERTREND EXPLORER / SCREENER screens the BUY and SELL signals (trend reversals) for 38 user defined different tickers in Tradingview charts.

Simply input the short name of the ticker in Tradingview that you want to screen.

Script is derived from zzzcrypto123 's work. Thanks for the permission letting me to use his logic.

Terminology explanation:

Confirmed Reversal: Supertrend reversal that happened in the last bar and cannot be repainted.

Potential Reversal: Supertrend reversal that might happen in the current bar but can also not happen depending upon the timeframe closing price.

Screener has also got a built in SuperTrend indicator which users can confirm the reversals on graphs.

Screener explores the 38 tickers in current graph's time frame and also in desired parameters of the SuperTrend indicator.

SUPERTREND INDICATOR:

STRATEGY version of SuperTrend Indicator:

SuperTrend is one of the most common ATR based trailing stop indicators.

In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA .

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier. The default values used while constructing a superindicator are 10 for average true range or trading period and three for its multiplier.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility .

The buy and sell signals are generated when the indicator starts plotting either on top of the closing price or below the closing price. A buy signal is generated when the ‘Supertrend’ closes above the price and a sell signal is generated when it closes below the closing price.

It also suggests that the trend is shifting from descending mode to ascending mode. Contrary to this, when a ‘Supertrend’ closes above the price, it generates a sell signal as the colour of the indicator changes into red.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on daily, weekly and hourly charts as well, but generally, it fails in a sideways-moving market.

Source function added to use the indicator as the ATR Trailing Stop indicator.

Just change source type hl2 to close.

different variations might be useful.

Search in scripts for "Trailing stop"

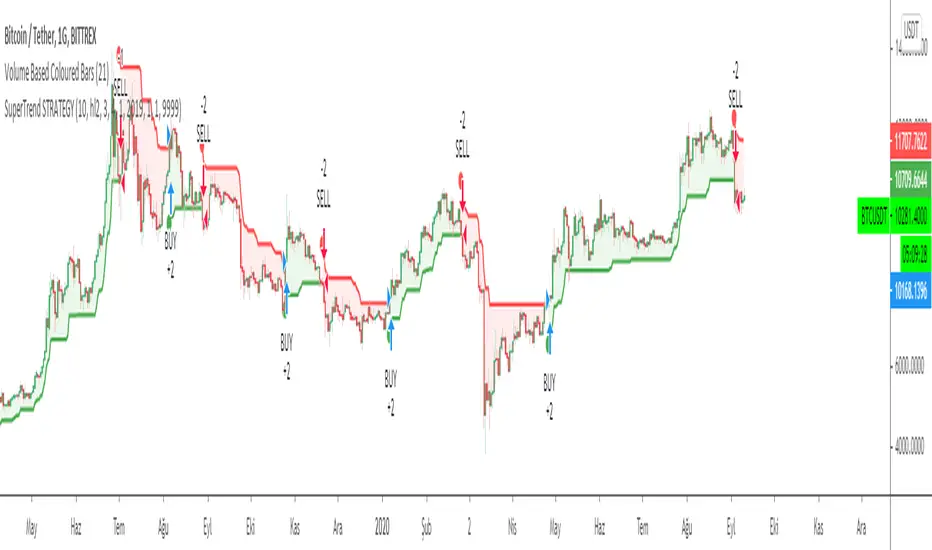

SuperTrend STRATEGYSTRATEGY version of SuperTrend Indicator:

SuperTrend is one of the most common ATR based trailing stop indicators.

In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA .

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier. The default values used while constructing a superindicator are 10 for average true range or trading period and three for its multiplier.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility .

The buy and sell signals are generated when the indicator starts plotting either on top of the closing price or below the closing price. A buy signal is generated when the ‘Supertrend’ closes above the price and a sell signal is generated when it closes below the closing price.

It also suggests that the trend is shifting from descending mode to ascending mode. Contrary to this, when a ‘Supertrend’ closes above the price, it generates a sell signal as the colour of the indicator changes into red.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on daily, weekly and hourly charts as well, but generally, it fails in a sideways-moving market.

Source function added to use the indicator as the ATR Trailing Stop indicator.

Just change source type hl2 to close.

different variations might be useful.

Coppock Curve StrategyThis strategy makes use of a not widely known technical indicator called "Coppock Curve".

The indicator is derived by taking a weighted moving average of the rate-of-change (ROC) of a market index such as the S&P 500 or a trading equivalent such as the S&P 500 SPDR ETF. For more info: (www.investopedia.com)

This strategy uses $SPY Coppock curve as a proxy to generate buy signals on other ETF's and stocks.

Buy signals are generated when the Coppock Curve crosses above zero, and sell signals are generated when it crosses below.

An optional, trailing stop loss is available, with default settings to 100% so that it does not currently affect the buy and sell signals solely generated by the Coppock Curve. But you may find adding a Trailing stop loss may improve results on certain ETF's/Stocks.

You may also change the symbol for which signals are generated for, default is $SPY.

The published example shows using this strategy on a leverage ETF $TQQQ w/ starting capital of 10k, w/ 10k per trade. Try it on other stocks such as $AAPL, $AMZN $NFLX ect... I have found it to be an effective strategy that has a favorable risk to reward profile.

Any questions, please let me know!

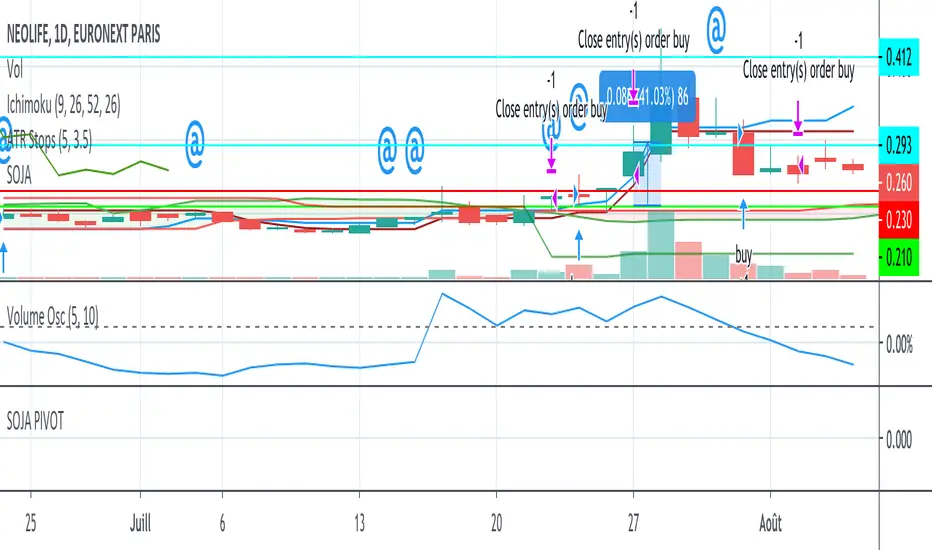

SOJA PIVOTStrategy using SOJA HUNTER indicator for buy and Pivot points for sell :

-1st TP at R1 with 25% shares

-2nd TP at R2 with 25% shares

SL using trailing stop.

CCI-RSI MR Indicators:

Bollinger Bands (20 period, 2σ)

RSI (14 period) and Simple moving average of RSI (5 period)

CCI (20 period)

SMA (5 period)

Entry Conditions:

Buy when:

Swing low (5) should be lower than the highest of lower BB (3 periods)

Both RSI crossover RSI_5 and CCI crossover -100 should have happened within last 3 candles (including the current candle)

Once all the above conditions are met, the close should be higher than SMA (5) within the next 3 candles

After condition 3 is satisfied, we enter the trade at next candle’s open

Stop loss will be at 1 tick lower than previous swing low

Sell when:

Swing high (5) should be higher than the lowest of upper BB (3 periods)

Both RSI crossunder RSI_5 and CCI crossunder 100 should have happened within last 3 candles (including the current candle)

Once all the above conditions are met, the close should be lower than SMA (5) within the next 3 candles

After condition 3 is satisfied, we enter the trade at next candle’s open

Stop loss will be at 1 tick higher than previous swing high

Exit Conditions:

Since it’s mean reversion strategy we’ll be having only 2 target exits with a trailing stop loss after target price 1 is achieved.

Target exit price 1 & 2 are decided based on the risk ‘R’ for each trade

Depending on the instrument and time frame a trailing stop loss of 0.5R or 1R has opted.

A stop limit is placed @Entry_price +- 2*ATR(20) to offset the risk of losing significantly more than 1xR in a trade

mForex - 3 Moving Average - Parabolic SARScript identifies the uptrend and downtrend according to the average price of the MA and PSAR lines.

Rules of sale:

- Open short positions when:

MA12 cuts MA26 and MA52 from the top.

PSAR dots on the price line

- Stop loss:

At the dots of PSAR and use Trailing Stop facing up

On the nearest peak

- Profit-taking: Corresponding ratio of R: R (1: 2)

- Open long positions when:

MA12 cuts MA26 and MA52 from the bottom.

PSAR dots below the price line

- Stop loss:

At the dots of PSAR and use Trailing Stop facing down

Below the nearest peak

- Profit-taking: Corresponding ratio of R: R (1: 2)

JMA + A2RTS + AlertsThe script is a combination of two high quality scripts Everget's JMA and Alex Grover's A2RTS script, all credit too them for the original code.

Additional thanks to Mango2Juice for the continued help as this is my first script published and it would not of been possible without the help.

The goal of this script is to allow for you to enter into trends and too keep you in them while maximizing profit.

Trade Conditions:

Buy Enter: when JMA goes from red to green and use yellow line (A2RTS) as a trail stop

Buy Exit: when A2RTS flips or JMA goes back to red

Sell Enter: when JMA goes from green to red and use yellow line (A2RTS) as a trail stop

Sell Exit: When A2RTS flips or JMA goes back to green

Alerts have also been added for when JMA changes color and when A2RTS flips

Please drop a comment below if this script is helpful or if you have any question

Once again this is my first script and I hope you all enjoy it.

Jsa Moving Average [CC]The Jsa Moving Average was created by George R. Arrington, Ph .D. (Stocks & Commodities V. 11:10 (427-431)) and it is an extremely simple formula but has very many great uses. For one thing it acts as support and resistance levels and it also acts like a trailing stop. It gives a wide enough berth during extended up or down trends to let you ride the wave up or down and when it gets close to the price it means that it is a choppy market. Buy when the indicator line is green and sell when it turns red.

Let me know if you would like to see me publish other indicators or if you want something custom done!

Note: I'm republishing this because the original script couldn't be found in searches so this will fix that.

TrenderTrender is a popular trailing stop indicator on the Bloomberg system and since I didn't have source code to work with, this is a close approximation of that indicator. Let me know if you spot any discrepancies and I will adjust accordingly.

This indicator is a trailing stop system along with a trend confirmation. When the blue line falls below the black line, that is a confirmation of a down trend and when it rises above the black line, it is a confirmation of an up trend. When the trender line is above the price, then that means the stock is in a general down trend and vice versa. I have color coded the trender line to show you when to buy or sell that stock to keep it easy.

This was a special request so let me know if you want to see more scripts from me or if you want something custom!

MAs & RSI strategy long onlyThis system originates from many articles by Enrico Malverti, Trading System, 2015.

Many trading systems are more stable if you use simple and not so innovative indicators, like exponential moving averages and Relative Strengthe index.

Differently by the original article:

- there is no ATR Filter, but we have introduced a Schaff Indicator. If you have multiple shares/commodities to choose, prefer what has a better value of Schaff;

- there is no fixed stop loss but a second moving average (fast), used as target. There are also Simple Mov Averages on lows (trailing stop loss for long) and a SMA on highs (trailing stop loss for short position).

Be careful, in the system only long case, because being short is not the reverse of being long (as stated in my blog)

SMA on highs are therefore only graphically put.

In this version, I’ve changed the “religious” use of EMAs (“sponsored by” Alexander Elder) to “ordinary” MAs: this because since simple moving averages measure all the factor in addition egual each one, this involve a sort of “offset” in the graph, while EMAs give a major “importance” to the last value (last close itself, you’re already considering): therefore this calculation may be counterproductive.

HOW TO OPERATE

BUY when prices crosses over SMAon long period (we suggest, however, sma long = Sma fast period = no. 11 for italian and european shares)

SELL when

prices go under SMA on lows (7 period), or under on SMA fast!

RSI crosses under level 70 or is higher than 75 (or 80, but in code there is 75)

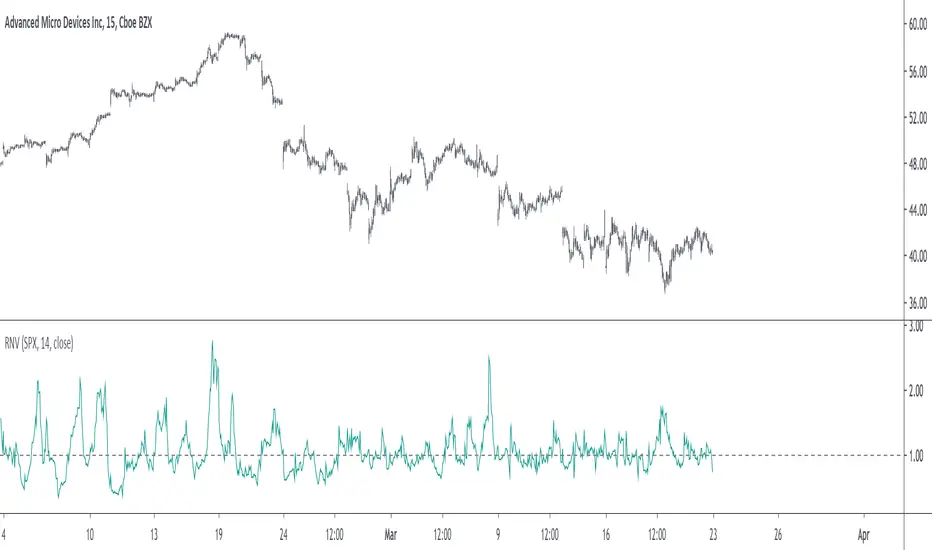

Relative Normalized VolatilityThere are plenty of indicators that aim to measure the volatility (degree of variation) in the price of an instrument, the most well known being the average true range and the rolling standard deviation. Volatility indicators form the key components of most bands and trailing stops indicators, but can also be used to normalize oscillators, they are therefore extremely versatile.

Today proposed indicator aim to compare the estimated volatility of two instruments in order to provide various informations to the user, especially about risk and profitability.

CALCULATION

The relative normalized volatility (RNV) indicator is the ratio between the moving average of the absolute normalized price changes value of two securities, that is:

SMA(|Δ(a)/σ(a)|)

―――――――――――

SMA(|Δ(b)/σ(b)|)

Where a and b are two different securities (note that notation "Δ(x)" refer to the 1st difference of x, and the "||" notation is used to indicate absolute value, for example "|x|" means absolute value of x) .

INTERPRETATION

The indicator aim tell us which security is more volatile between a and b , with a value of the indicator greater than 1 indicating that a is on average more volatile than b over the last length period, while a value lower than 1 indicating that the security b is more on average volatile than a .

The indicator use the current symbol as a , while the second security b must be defined in the setting window (by default the S&P500). Risk and profitability are closely related to volatility, as larger price variations could potentially mean larger losses (but also larger gains), therefore a value of the indicator greater than 1 can indicate that it could be more risked (and profitable) to trade security a .

RNV using AMD (top) volatility against Intel (bottom) volatility.

RNV using EURUSD (top) volatility against USDJPY (bottom) volatility.

Larger values of length will make the indicator fluctuate less often around 1. You can also plot the logarithm of the ratio instead in order to have the indicator centered around 0, it will also help make values originally below 1 have more importance in the scale.

POSSIBLE ERRORS

If you compare different types of markets the indicator might return NaN values, this is because one market might be closed, for example if you compare AMD against BTCUSD with the indicator you will get NaN values. If you really need to compare two markets then increase your time frame, else use an histogram or area plot in order to have a cleaner plot.

CONCLUSION

An original indicator comparing the volatility between two securities has been presented. The choice of posting a volatility indicator has been made by my twitter followers, so if you want to decide which type of indicator i should do next make sure to check my twitter to see if there are polls available (i should do one after every posted indicator).

ATA v4 StrategyAta strategy is include 3 different time frame = MTF

2 different moving average =MA

Oversold/overbought for relative strength index =RSI

Strategy exit for trailing stop loss %2 =TSL

MTF like 1 day, 4h and 5 min, between 2 moving averages like fibo numbers 21 and 34. Also strategy test for oversold up to 60 and overbought under the 25 with RSI. Stratefy exit include trailing stop loss %2 persantage for max. gain. It was created by XMAXPRO. This system is open to development.

Donchian Breakout StrategyThis strategy buys when the Donchian Channel is broken to the upside and uses the lower Donchian Channel line as a trailing stop. You can also choose to use a moving average as a filter to keep you out of trades that are counter trend.

You can also configure which dates you want to backtest, so you can see how this behaves over specific time frames and market cycles.

Extended Recursive Bands - Maximum Efficiency With Extra OptionsIntroducing A New Calculation For Efficient Bands Calculation !

Here it is ! The Recursive Bands Indicator, an indicator specially created to be extremely efficient, i think you already know that calculation time is extra important in algorithmic trading, and this is the principal motivation for the creation of the proposed indicator. Originally described in my paper "Pierrefeu, Alex (2019): Recursive Bands - A New Indicator For Technical Analysis" , the indicator framework has been widely used in my previous uploaded indicators, however it would have been a shame to not upload it, however user experience being a major concern for me, i decided to add extra options, which explain the term "extended".

On The Indicator Calculation

You can skip this part if it doesn't interest you. The calculation of the indicator is based on recursion, but i want to explain the mathematical formula described in the paper.

I've seen some users trying to remake it from the calculations, however there was always something weird, and i understand, mathematical notations are always a bit weird, even myself don't always write them correctly/understand them, however this one is relatively simple to understand.

First lets explain each elements of the calculation :

α = smoothing constant, or 2/(length+1)

max/min = maximum and minimum function, max return the greatest input value while min return the lowest one, for example :

max(4,2) = 4 while min(4,2) = 2

the "||" notation mean taking the absolute value, for example : |-1| = abs(-1) = 1

The calculation after the max/min function is called the correction factor, and is the core of the indicator. The last two variables are just here to provide an initial value for upper and lower, basically when we start our calculations we will assign the value of the closing price for upper and lower.

The motivation behind using a smoothing constant in range of (0,1) was to tell the reader that the indicator is easily made adaptive, this is what i did on my adaptive trailing stop indicator by using the efficiency ratio as smoothing variable, the user can use 1/length instead of the provided calculation for alpha.

If you interested on the indicator main logic, it is actually really simple, by using upper = max(price,upper) and lower = min(price,lower) we would get the maximum/minimum price value at time t , therefore upper can only be greater or equal than its precedent value, while lower can only be lower or equal than its precedent value, in order to fix that we subtract/sum upper/lower with a value, this allow the upper band to be lower than its precedent value and lower to be greater than its precedent value, this is the role of the correction factor.

The Indicator

The indicator display one upper and one lower band, every common usages applied to bands indicators such as support/resistance, breakout, trailing stop...etc, can also be applied to this one. length control how reactive the bands are, higher values of length will make the bands cross the price less often.

In order to provide more flexibility for the user i added the option to use various methods for the calculation of the indicator, therefore the indicator can use the average true range, standard deviation, average high-low range, and one totally exclusive method specially designed for this indicator.

Classic Method

This option make the indicator use its classical calculation, this is the most efficient method of all.

Atr Method (atr)

This method use the average true range as correction factor, notice that lower values of length can still produce wide band.

Standard Deviation Method (stdev)

This method use a biased estimate of the standard deviation as correction factor.

The method produce smoother bands that converge more slowly toward the price in comparison with the classic correction factor.

Average High-Low Range Method (ahlr)

This method use the average of the high-low range as correction factor, extremely similar to the average true range.

Rising Falling Volatility (rfv) Method

A new method created for this indicator, this correction factor use the absolute prices changes when price value is greater/lower than any length past values of the price, this allow to have more boxy shaped bands, work best with greater values of length.

The bands can be in contact with this method, a possible fix in the future.

Conclusion

The recursive band indicator is one of my greatest indicators in my opinion (i would love to have yours), as you can see the idea behind it is extremely simple and allow for a super efficient band indicator, which was the original motivation behind it, in order to provide more fun for the users i also added more option for the correction factor, this allow the user to be creative and not get stuck with the original calculation.

Like the trend step indicator family we have almost ended our series on the recursive band framework, 1 more trailing stop will be added in the future, and then we'll have more "boring" stuff until i find something cool again, it shouldn't be long ;)

Thanks for reading !

G-Channels - Efficient Calculation Of Upper/Lower ExtremitiesIntroduction

Channels indicators are widely used in technical analysis, they provide lot of information. In general, technical indicators giving upper/lower extremities are calculated by adding/subtracting a volatility component to a central tendency estimator. This is the case with Bollinger bands, using the rolling standard deviation as volatility estimator and the simple moving average as central tendency estimator, or the Keltner channels using the exponential moving average and the average true range.

Lots and lots and lots (i can go on) of those indicators have been made, they only really need a central tendency estimator, which can be obtained from pretty much any filter, however i find interesting to focus on the efficiency of those indicators, therefore i propose a super efficient channel indicator using recursion. The average resulting from the upper/lower extremity of the indicator provide a new efficient filter similar to the average highest/lowest.

The calculation - How Does It Works

Efficiency is often associated to recursion, this would allow us to use past output values as input, so how does the indicator is calculated? Lets look at the upper band calculation :

a := max(src,nz(a(1))) - nz(a(1) - b(1))/length

src is the closing price, a is upper extremity, b is the lower one. Here we only need 3 values, the previous values of a and b and the closing price. Basically a := max(src,nz(a(1))) mean :

if the closing price is greater than the precedent value of a then output the closing price, else output the precedent value of a

therefore a will never be inferior to its precedent value, this is useful for getting the maximum price value in our dataset however its not useful to make an upper band, therefore we subtract this to a correction factor defined as the difference between a and b , this force the upper band to have lower values thus acting like a band without loosing its "upper" property, a similar process is done with the lower band.

Of course we could only use 2 values for making the indicator, thus ending with :

a := max(src,nz(a(1))) - nz(abs(close - a(1))/length

In fact this implementation is the same as the one proposed in my paper "Recursive Bands - A New Indicator For Technical Analysis", its also what i used for making the indicator "Adaptive Trailing Stop", this would be more efficient but i used the difference between the upper and lower extremities for a reason.

The Central tendency Estimator

This is the reason why i didn't implemented a more efficient version. Basically this central tendency estimator is just the average between the upper and lower extremities, it behave like the average of the highest/lowest over length period, its central plot in the Donchian channel indicator. Below is a comparison of both with length = 100 :

But why is our average so "boxy"? The extremities are not boxy, so why the average is sometimes equal to its previous value? Explain!

Its super easy to understand, imagine two lines, if their absolute change is the same and they follow an opposite direction, then their average is constant.

the average of the green and red line is the orange line. If both lines follow the same direction then their average will also follow this direction.

When both extremities follow the same direction, the average will also do the same, when both follow an opposite direction then the average will be equal to its precedent value, this is also due to the fact that both extremities are based on the same correction factor (a-b) , else the average wouldn't act that way, now you understand why i made this choice.

Conclusion

I proposed an efficient implementation of a channel indicator that provide an interesting central tendency estimator. This simple implementation would allow for tons of interesting concepts, some of my indicators use a similar approach and allow for great outputs, you'll see them soon enough. I hope this indicator find its use in the community, remember to ask before using this indicator in a script you want to publish.

Thanks for reading !

If you want to discuss about anime stuff send me a pm but don't do it in the commend section.

Peterbolic SARThe Peterbolic SAR indicator is based on Peter Brandt's 3 Day Trailing Stop Rule. The yellow triangles indicate setup candles, and the green and red triangles represent trigger candles to buy and sell, respectively.

Sawcruhteez asked me to create the code for this SAR. Gabriel Harber came up with the name for the SAR. Peter Brandt gave his permission to use his name.

For more information, see Sawcruhteez Streamz: Live Coaching Sessionz with Gabriel Harber - Trading Peterbolic SAR

and Peter Brandt's original description of the 3DTSR

4 JMA Crossover Strategy (ps4)This is a PS4 update to my previous 4 JMA strategy that received many likes. In this and several recent strategies I use a simplified strategy setup, featuring trailing stops with very tiny increments. This is done intentionally in order to boost performance to the limit, so that to pinpoint that limit. Strategies with performance of about 90% or above are regarded as viable. Incorporating various overhead factors such as transaction costs, broker's spread, slippage, etc. at this stage creates too much 'noise' with the end result of losing the sight of the forest behind the trees.)) In practice, I disable the 'Use Strategy Setup' option and fine-tune parameters the way I want.

Tested security: EURUSD . Tested TF: 3m

Scaled Normalized Vector Strategy, ver.4.1This modification of the Scaled Normalized Vector Strategy uses trailing stops and is optimized for lower TFs.

Kaufman Adaptive BandsIntroduction

Bands are quite efficient in technical analysis, they can provide support and resistance levels, provide breakouts points, trailing stop loss/take profits positions and can show the current market volatility to the user. Most of the time bands are made from a central tendency estimator like a moving average plus/minus a volatility indicator. Therefore bands can be made out of pretty much everything thus allowing for any kind of flavors.

So i propose a band indicator made from a Kaufman adaptive moving average using an estimate of the standard deviation.

Construction

The Kaufman moving average is an exponential averager using the efficiency ratio as smoothing variable, length control the period of kama and in order to provide more smoothness a power parameter has been introduced, higher values of power will return smoother results.

The volatility indicator is made from a biased estimation of the standard deviation by using the square root of the mean of the square minus the square of the mean method, except that we use kama instead of a mean.

The bands are made by adding/subtracting this volatility indicator with kama.

How To Use

The ability of the indicator to adapt to the current market state is what makes him a great tool for avoiding major exposition during ranging market, therefore the indicator will have a greater motion during trending market, or more simply the bands will move during trending markets while staying "flat" during ranging ones. Therefore the indicator might be more suited to breakouts, even if some cases will return what where turning points, this is particularly true during ranging markets.

Of course the efficiency ratio is not an "unbiased" trend metric indicator, it can consider high volatility markets as trending markets. Its one of his downsides.

High values of power will create smoother bands.

When using a low power parameter use an higher mult. In general using a low power value will make the bands move more freely as well as making them closer to each others.

Conclusion

At least the indicator is really nice to the eyes when using high power values, its ability to adapt to the market is a great addition to other more classical bands indicators, i also introduced a volatility estimator based on kama, some might have used the following estimation : kama(abs(price - kama)) which would have created a slower result. A trailing stop might be made from it if i see request about such addition.

If you are curious here are some more images of the indicator performing on different markets. Thanks for reading !

Renko Plot StrategyThis strategy lets you plot Renko open and close values, based on your preferred Renko size brick, on normal candle chart. You can use it on any timeframe, define your preferred brick size and trailing stop.

Modified Gann HiLo ActivatorIntroduction

The gann hilo activator is a trend indicator developed by Robert Krausz published into W. D. Gann Treasure Discovered: Simple Trading Plans for Stocks & Commodities . This indicator crate a trailing stop aiming to show the direction of the trend.

This indicator is fairly easy to compute and dont require lot of skills to understand. First we calculate the simple moving average of both price high and price low, when the close price is higher than the moving average of the price high the indicator return the moving average of the price low, else the indicator return the moving average of the price high if the close price is lower than the moving average of the price low.

My indicator add a different calculation method in order to avoid whipsaw trades as well as adding significance to the moving average length. A Median method has been added to provide more robustness.

The Indicator

The indicator is a simple trailing stop aiming to show the direction of the trend. The indicator use a different source instead of the price high/low for its calculation. The first method is the "SMA" method which like the classic hilo indicator use a simple moving average for the calculation of the indicator.

Sma Method with length = 25

The "Median" use a moving median instead of a simple moving average, this provide more robustness.

Median Method with length = 25

The shape is less curved and the indicator can sometimes avoid whipsaw with high's length periods.

Mult Parameter

The mult parameter is a parameter set to be lower or equal to 1 and greater or equal to 0. High values allow the indicator to be far from the price thus avoiding whipsaw trades, lower ones lower the distance from the price. A mult parameter of 0.1 approximate the original hilo indicator.

In blue the indicator with mult = 0.1 and in radical red the original hilo activator.

Conclusion

The modifications allow more control over the indicator as well as adding more robustness while the original one is destined to fail when market price is more complex.

Thanks for reading :)

For any questions/suggestions feel free to pm me

Generalized SSL by Vts// Generalized SSL:

// This is the very first time the SSL indicator, whose acronym I ignore, is on Tradingview.

// It is based on moving averages of the highs and lows.

// Similar channel indicators can be found, whereas

// this one implements the persistency inside the channel, which is rather tricky.

// The green line is the base line which decides entries and exits, possibly with trailing stops.

// With respect to the original version, here one can play with different moving averages.

// The default settings are (10,SMA)

//

// Vitelot/Yanez/Vts March 2019

Chandelier ExitThis is a redesign of the Chandelier Exit indicator. It removes stupid transitions between Chandelier Exit' states and highlights initial points for both lines.

This indicator was originally developed by Charles Le Beau and popularized by Dr. Alexander Elder in his book "Come Into My Trading Room: A Complete Guide to Trading" (2002).

In short, this is a trailing stop-loss based on the Average True Range (ATR).